Here’s my re-write of the chapter on money again. I must stress that this is now going into an edit process so it will come out looking slightly different. Quite a bit of material got dumped (which really hurts when you like it). Otherwise it was a matter of better signposting, starting with the economy and then moving into money and constantly teasing out the digital. Sorry about the layout, it’s gone rather haywire. (BTW, I’ve added a few links, which obviously won’t appear in any paper versions of this chapter).

—

The Economy and Money: Is digital money making us more careless?

The idea of the future being different from the present is so repugnant to our conventional modes of thought and behaviour that we, most of us, offer a great resistance to acting on its practice. John Maynard Keynes, economist

Networks of inequality

A few years ago I was walking down a street in West London when a white van glided to a halt opposite. Four men stepped out and slowly slid what looked like a giant glass coffin from the rear. Inside it was a large shark.

The sight of a live shark in London was slightly surreal, so I sauntered over to ask what was going on. It transpired that the creature in question was being installed in an underground aquarium in the basement of a house in Notting Hill. This secret subterranean lair should, I suppose, have belonged to Dr Evil. To local residents opposing deep basement developments it probably did. A more likely candidate might have been someone benefiting from the digitally networked nature of global finance. A partner at Goldman Sachs, perhaps. This is the investment bank immortalised by Rolling Stone magazine as: ‘a great vampire squid wrapped around the face of humanity.’ Or possibly the owner was the trader known as the London Whale, who lost close to six billion dollars in 2012 for his employer, JP Morgan, by electronically betting on a series of highly risky and somewhat shady derivatives known as Credit Default Swaps.

London real estate had become a serious place to stash funny money, so maybe the house belonged to a slippery individual dipping their fingers into the bank accounts of a corrupt foreign government or international institution. In the words of William Gibson, the former sci-fi writer, London is: “Where you go if you successfully rip off your third world nation.”

Whichever ruthless predator the house belonged to, something fishy was underfoot. My suspicion was that it had to do with unchecked financial liberalisation, but also how the digital revolution was turning the economy into a winner-takes-all online casino.

The shift of power away from locally organised labour to globally organised capital has been occurring for a while, but the recent digital revolution has accelerated and accentuated this. Digitalisation hasn’t directly enabled globalisation, but it certainly hasn’t restrained it either and one of its negative side effects has been a tendency toward polarisation, both in terms of individual incomes and market monopolies.

Throughout most of modern history, around two-thirds of the money made in developed countries was typically paid as wages. The remaining third was paid as interest, dividends or other forms of rent to the owners of capital. But since 2000, the amount paid to capital has increased substantially while that paid to labour has declined, meaning that real wages have remained flat or fallen for large numbers of people.

The shift toward capital could have an innocent analogue explanation. China, home to an abundant supply of low-cost labour, has pushed wages down globally. This situation could soon reverse, as China runs out of people to move to its cities, their pool of labour shrinks, due to ageing, and Chinese wages increase. Alternatively, low-cost labour may shift somewhere else — possibly Africa. But another explanation for the weakened position of human labour is that humans are no longer competing against each other, but against a range of largely unseen digital systems. It is humans that are losing out. A future challenge for governments globally will therefore be the allocation of resources (and perhaps taxes) between people and machines given that automated systems will take on an increasing number of previously human roles and responsibilities.

Same as it ever was?

Ever since the invention of the wheel we’ve used machines to supplement our natural abilities. This has always displaced certain human skills. And for every increase in productivity and living standards there’ve been downsides. Fire cooks our food and keeps us warm, but it can burn down our houses and fuel our enemy’s weapons. During the first industrial revolution machines further enhanced human muscle and then we outsourced further dirty and dangerous jobs to machines. More recently we’ve used machines to supplement our thinking by using them for tedious or repetitive tasks.

What’s different now is that digital technologies, ranging from advanced robotics and sensor networks to basic forms of artificial intelligence and autonomous systems, are threatening areas where human activity or input was previously thought essential or unassailable.In particular, software and algorithms with near-zero marginal cost are now being used for higher-order cognitive tasks. This is not digital technology being used alongside humans, but as an alternative to them. This is not digital and human. This is digital instead of human.

Losing an unskilled job to an expensive machine is one thing, but if highly skilled jobs are lost to cheap software where does that leave us? What skills do the majority of humans have left to sell if machines and automated systems start to think? You might be feeling pretty smug about this because you believe that your job is somehow special or terribly difficult to do, but the chances are that you are wrong, especially when you take into account what’s happening to the cost and processing power of computers. It’s not so much what computers are capable of now, but what they could be capable of in ten or twenty years time that you should be worried about.

I remember ten or so years ago reading that if you index the cost of robots to humans with 1990 as the base (1990=100) the cost of robots had fallen from 100 to 18.5. In contrast, the cost of people had risen to 151. Der Spiegel, a German magazine, recently reported that the cost of factory automation relative to human labour had fallen by 50 per cent since 1990.

Over the shorter term there won’t be much to worry about. Even over the longer term there’ll still be jobs that idiot savant software won’t be able to do very well — or do at all. But unless we wake up to the fact that we’re training people to compete head on with machine intelligence there’s going to be trouble eventually. This is because we are filling peoples’ heads with knowledge that’s applied according to sets of rules, which is exactly what computers do. We should be teaching people to do things that these machines cannot. We should be teaching people to constantly ask questions, find fluid problems, think creatively and act empathetically. We should be teaching high abstract reasoning, lateral thinking and interpersonal skills. If we don’t a robot may one day come along with the same cognitive skills as us, but costs just $999. That’s not $999 a month, that’s $999 in total. Forever. No lunch breaks, holidays, childcare, sick pay or strike action, either. How would you compete with that?

If you think that’s far fetched, Foxconn, a Chinese electronics assembly company, is designing a factory in Chengdu that’s totally automated — no human workers involved whatsoever. I’m fairly sure we’ll eventually have factories and machines that can replicate themselves too, including software that writes its own code and 3D printers that can print other 3D-printers. Once we’ve invented machines that are smarter than us there is no reason to suppose that these machines won’t go on to invent their own machines – which we then won’t be able to understand – and so on ad infinitum. Let’s hope these machines are nice to us.

It’s funny that our obsessive compulsive addiction to machines, especially mobile devices, is currently undermining our interpersonal skills and eroding our abstract reasoning and creativity, when these skills are exactly what we’ll need to compete against the machines.

But who ever said that the future couldn’t be deeply ironic.

There are more optimistic outcomes of course. Perhaps the productivity gains created by these new technologies will eventually show up and the resulting wealth will be more fairly shared. Perhaps there’ll be huge cost savings made in healthcare or education. Technologically induced productivity gains may offset ageing populations and shrinking workforces too. It’s highly unlikely that humans will stop having interpersonal and social needs and even more unlikely that the delivery of all these needs will be within the reach of robots. In the shorter term it’s also worth recalling an insightful comment attributed to NASA in 1965, which is that: “Man is the lowest-cost, all-purpose computer system which can be mass-produced by unskilled labour.” But if the rewards of digitalisation are not equitable or designers decide that human agency is dispensable or unprofitable then a bleaker future may emerge, one characterised by polarisation, alienation and discomfort.

Money for nothing

Tim Cook, the CEO of Apple, once responded to demands that Apple raise its return to shareholders by saying that his aim was not to make more profit. His aim was to make better products, from which greater financial returns would flow. This makes perfect sense to anyone except speculators carelessly seeking short-term financial gains at the expense of broader measures of benefit or value. As Jack Welch, the former CEO of General Electric once said: “Shareholder value is the dumbest idea in the world.”

It was Plato who pointed out that an appetite for more could be directly linked with bad human behaviour. This led Aristotle to draw a black and white distinction between the making of things and the making of money. Both philosophers would no doubt have been disillusioned with high frequency trading algorithms – algorithms being computer programs that follow certain steps to solve a problem or react to an observed situation. In 2013, algorithms traded $28 million worth of shares in 15 milliseconds after Reuters released manufacturing data milliseconds early. Doubtless money was made here, but for doing what?

Charles Handy, the contemporary philosopher, makes a similar point in his book The Second Curve that when money becomes the point of something then something goes wrong. Money is merely a secure way to hold or transmit value (or ‘frozen desire’ as someone more poetically put it). Money is inherently valueless unless exchanged for something else. But the aim of many digital companies appears to be to make money by selling themselves (or their users) to someone else. Beyond this their ambition appears to be market disruption by delivering something faster or more conveniently than before. But to what end ultimately? What is their great purpose? What are they for beyond saving time and delivering customers to advertisers?

In this context, high frequency trading is certainly clever, but it’s socially useless. It doesn’t make anything other than money for small number of individuals. Moreover, while the risks to the owners of the algorithms are almost non-existent, this is not generally the case for the society as a whole. Huge profits are privatised, but huge losses tend to be socialised.

Connectivity has multiple benefits, but linking things together means that any risks are linked with the result that systemic failure is a distinct possibility. So far we’ve been lucky. Flash Crashes such as the one that occurred on 6 May 2010 have been isolated events. On this date high-speed trading algorithms decided to sell vast amounts of stocks in seconds, causing momentary panic. Our blind faith in the power and infallibility of algorithms makes such failures more likely and more severe. As Christopher Steiner, author of Automate: How Algorithms Came to Rule Or World writes: ‘We’re already halfway towards a world where algorithms run nearly everything. As their power intensifies, wealth will concentrate towards them.’ Similarly, Nicholas Carr has written that: ‘Miscalculations of risk, exacerbated by high-speed computerised trading programs, played a major role in the near meltdown of the world’s financial system in 2008.’ Digitalisation helped to create the sub-prime mortgage market and expanded it at a reckless rate. But negative network effects meant that the market imploded with astonishing speed, partly because financial networks were able to spread panic as easily as they had been able to transmit debt. Network effects can create communities and markets very quickly, but they can destroy them with velocity and ferocity too. Given the world’s financial markets, which influence our savings and pensions, are increasingly influenced by algorithms, this is a major cause for concern. After all, who is analysing the algorithms that are doing all of the analysing?

Out of sight and out of mind

Interestingly, it’s been shown that individuals spend more money when they use digital or electronic money rather than physical cash. Because digital money is somehow invisible or out of sight our spending is less considered or careful. And when money belongs to someone else, a remote institution rather than a known individual for instance, any recklessness and impulsiveness is amplified. Susan Greenfield, the neuroscientist, has even gone as far as to link the 2008 financial crisis to digitalisation because digitalisation creates a mindset of disposability. If, as a trader, you have grown up playing rapid-fire computer games in digital environments you may decide that similar thrills can be achieved via trading screens without any direct real-world consequences.

You can become desensitised. Looking at numbers on a screen it’s easy to forget that these numbers represent money and ultimately people. Having no contact with either can be consequential. Putting controls on computers can make matters worse because we tend to take less notice of information when it’s delivered on a screen amid a deluge of other digital distractions.

Carelessness can have other consequences too. Large basement developments such as the one I stumbled into represent more than additional living space. They are symbolic of a gap that’s opening up between narcissistic individuals who believe that they can do anything they want if they can afford it and others who are attempting to hang on to some semblance of physical community. A wealthy few even take pleasure seeing how many local residents they can upset, as though it were some kind of glorious computer game. Of course, in the midst of endless downward drilling and horizontal hammering, the many have one thing that the few will never have, which is enough.

Across central London, where a large house can easily cost ten million pounds, it is not unusual for basement developments to include underground car parks, gyms, swimming pools and staff quarters, although the latter are technically illegal. It’s fine to stick one of nature’s most evolved killing creatures 50 feet underground, but local councils draw a line in the sand with Philippino nannies.

The argument for downward development is centred on the primacy of the individual in modern society. It’s their money (digital or otherwise) and they should be allowed to do whatever they like with it. There isn’t even a need to apologise to neighbours about the extended noise, dirt and inconvenience. The argument against such developments is that it’s everyone else’s sanity and that neighbourhoods and social cohesion rely on shared interests and some level of civility and cooperation.

If people start to build private cinemas with giant digital screens in basements this means they aren’t frequenting public spaces such as local cinemas, which in turn impacts on the vitality of the area. In other words, an absence of reasonable restraint and humility by a handful of self-centred vulgarians limits the choices enjoyed by the broader community. This isn’t totally the fault of digitalisation, far from it, but the idea that an individual can and should be left alone to do or say what they like is being amplified by digital technology. This is similar, in some respects, to the way in which being seated securely inside a car seems to bring out the worst in some drivers’ behaviour toward other road users. Access to technology, especially technology that’s personal and mobile, facilitates remoteness, which in turn reduces the need to interact physically or consider the feelings of other human beings. Remote access, in particular, can destroy human intimacy and connection, although on the plus side such technology can be used to expose or shame individuals that do wrong in the eyes of the broader community.

In ancient Rome there was a law called Lex Sumptuaria that restrained public displays of wealth and curbed the purchasing of luxury goods. Similar sumptuary laws aimed at superficiality and excess have existed in ancient Greece, China, Japan and Britain. Perhaps it’s time to bring these laws back — or at least to levy different rates of tax or opprobrium on immodest or socially divisive consumption or on digital products that damage the cohesiveness of the broader physical community.

Income polarisation and inequality aren’t new. Emile Zola, the French writer, referred to rivers of money: ‘Corrupting everyone in a fever of speculation’ in mid-19th Century Paris. But could it be that a fever of digital activity is similarly corrupting? Could virtualisation and personalisation be fraying the physical bonds that make us human and ultimately hold society together? What’s especially worrying here is that studies suggest that wealth beyond a certain level erodes empathy for other human beings. Perhaps the shift from physical to digital interaction and exchange is doing much the same thing.

But it’s not just the wealthy that are withdrawing physically. Various apps are leading to what some commentators are calling the shut in economy. This is a spin-off from the on-demand economy, whereby busy people, including those that work from home, are not burdened by household chores. But perhaps hardly ever venturing outside is as damaging as physically shutting others out. As one food delivery service, Door Dash, cryptically says: “Never leave home again”.

Where have all the jobs gone?

I’d like to move on to consider some other aspects of digital exchange, but before I do I’d like to dig a little deeper into the question of whether computers and automated systems are creating or destroying wealth and what happens to any humans that become irrelevant to the needs of the on-demand digital economy.

The digitally networked nature of markets is making some people rich, but also spreading wealth around far more than you might think. Globally, the level of inequality between nations is lessening and so too is extreme poverty. In 1990, for example, 43 per cent of people in emerging markets lived in extreme poverty, defined as existing on less than $1 per day. By 2010, this figure had shrunk to 21 per cent. Or consider China. In 2000, around 4 per cent of Chinese households were defined as middle class. By 2012, this had increased to two-thirds and by 2022, it’s predicted that almost half (45%) of the Chinese population will be middle class, defined as having annual household incomes of between US $9,000 and $16,000. This has more to do with demographics and deregulation than digitalisation, but by accident or design global poverty has been reduced by half in 20 years. Nevertheless, the gap between the highest and lowest earning members of society is growing and is set to continue with the onward march of digital networks. As the novelist Jonathan Franzen says: “The internet itself is in an incredibly elitist concentrator of wealth in the hands of the few while giving the appearance of voice and the appearance of democracy to people who are in fact being exploited by the technologies.”

If you have something that the world feels it needs right now it’s now possible to make an awful lot of money very quickly, especially if the need can be transmitted digitally. However, the spoils of regulatory and technological change are largely being accrued by people who are highly educated and internationally minded. If you are neither of these things then you are potentially destined for low-paid, insecure work, although at least you’ll have instant access to free music, movie downloads and computer games to pass the time until you die.

There’s been much discussion about new jobs being invented, including jobs we can’t currently comprehend, but most current jobs are fairly routine and repetitive and therefore ripe for automation. Furthermore, it’s unrealistic to expect that millions of people can be quickly retrained and reassigned to do jobs that are beyond the reach of robots, virtualisation and automation. Losing a few thousand jobs in car manufacturing to industrial robots or Amazon wiping out a bookshop is one thing, but what happens if automation removes vast swathes of employment across the globe? What if half of all jobs were to disappear? Moreover, if machines do most of the work how will most people acquire enough money to pay for the things that the machines make, thereby keeping the machines in employment? Maybe we should tax robots instead of people?

In theory the internet should be creating jobs. In the US between 1996 and 2005 it looked like it might. Productivity increased by around 3 per cent and unemployment fell. But by 2005 (i.e. before the global recession) this started to reverse. Why might this be so? According to McKinsey & Company, a firm of consultants, computers and related electronics, information industries and manufacturing contributed about 50 per cent of US productivity increases since 2000 ‘but reduced (US) employment by 4,500,000 jobs.’

Perhaps productivity gains will take time to come. This is a common claim of techno-optimists and the authors of the book, Race Against the Machine. Looking at the first industrial revolution, especially the upheavals brought about by the great inventions of the Victorian era, they could have a point.

But it could be that new technology, for all its power, can’t compete with simple demographics and sovereign debt. Perhaps, for all its glitz, computing just isn’t as transformative as stream power, railroads, electricity, postage stamps, the telegraph or the automobile. Yes we’ve got Facebook, Snapchat and Rich Cats of Instagram, but we haven’t set foot on the moon since 1969 and traffic in many cities moves no faster today than it did 100 years ago. It is certainly difficult to argue against certain aspects of technological change. Between 1988 and 2003, for example, the effectiveness of computers increased a staggering 43,000,000-fold. Exponentials of this nature must be creating tectonic shifts somewhere, but where exactly?

Is efficiency a good measure of value?

In its heyday, in 1955, General Motors employed 600,000 people. Today, Google, a similarly iconic American company, employs around 50,000. Facebook employs about 6,000. More dramatically, when Facebook bought Instagram for $1 billion in 2012, Instagram had 30,000,000 users, but employed just 13 people full time. At the time of writing, Whatsapp had just 55 employees, but a market value exceeding that of the entire Sony Corporation. This forced Robert Reich, a former US treasury Secretary, to describe Whatsapp as: ‘everything that’s wrong with the US economy.’ This isn’t because the company is bad — it’s because it doesn’t create jobs. Another example is Amazon. For each million dollars of revenue that Amazon makes it employs roughly one person. This is undoubtedly efficient, but is it desirable? Is it progress? These are all examples of the dematerialisation of the global economy, where we don’t need as many people to produce things, especially when digital products and services have a near zero marginal cost and where customers can be co-opted as free click-workers that don’t appear on any balance sheet.

A handful of people are making lots of money from this and when regulatory frameworks are weak or almost non-existent and geography becomes irrelevant these sums tend to multiply. For multinational firms making money is becoming easier too, not only because markets are growing, but because huge amounts of money can be saved by using information technology to co-ordinate production and people across geographies.

Technology vs. psychology

If a society can be judged by how it treats those with the least then things are not looking good. Five minutes walk from the solitary shark and winner takes all mentality you can find families that haven’t worked in three generations. Many of them have given up hope of ever doing so. They are irrelevant to a digital economy or, more specifically, what Manuel Castells, a professor of sociology at the University of California at Berkeley, calls ‘informational capitalism.’

Similarly, Japan is not far off a situation where some people will retire without ever having worked and without having moved out of the parental home. In some ways Japan is unique, for instance its resistance to immigration. But in other ways Japan offers a glimpse of what can happen when a demographic double-whammy of rapid ageing and falling fertility means that workforces shrink, pensions become unaffordable and younger generations don’t enjoy the same dreams, disposable incomes or standards of living as their parents.

Economic uncertainty and geo-political volatility, caused partly by a shift from analogue to digital platforms, can mean that careers are delayed, which delays marriage, which feeds through to low birth rates, which lowers GDP, which fuels more economic uncertainty. This is all deeply theoretical, but the results can be hugely human. If people don’t enjoy secure employment, housing or relationships, what does this do to their physical and especially psychological state? I expect that a negative psychological shift could be the next big thing we experience unless a coherent ‘we’ emerges to challenge some of the more negative aspects of not only income inequality, but the lack of secure and meaningful work for the less talented, the less skilled and less fortunate.

A few decades ago people worked in a wide range of manufacturing and service industries and collected a secure salary and benefits. But now, according to Yochai Benkler, a professor at Harvard Law School, the on-demand digital economy is efficiently connecting people selling certain skills to others looking to buy. This sounds good. It sounds entrepreneurial. It sounds efficient and flexible and is perhaps an example of labour starting to develop its own capital. But it’s also, potentially, an example of mass consumption decoupling from large-scale employment and of the fact that unrestrained free-markets can be savagely uncompromising.

Of course, unlike machines, people can vote and they can revolt too, although I think that passive disaffection and disenfranchisement are more likely. One of the great benefits of the internet has been the ease with which ideas can be transmitted across the globe, but ideas don’t always turn into actions. The transmission of too much data or what might be termed ‘too much truth’ is also resulting in what Castells calls: ‘informed bewilderment.’ This may sound mild, but if bewilderment turns into despair and isolation there’s a chance this could feed into fundamentalism, especially when the internet is so efficient at hosting communities of anger and transmitting hatred.

There is also evidence emerging that enduring physical hardship and mental anguish not only create premature ageing, which compromises the immune and cardiovascular system, but that this has a lasting legacy for those people having children. This is partly because poorer individuals are more attuned to injustice, which feeds through to ill health and premature ageing, and partly because many of the subsequent diseases can be passed on genetically. But perhaps it’s not relative income levels per se that so offend, but the fact that it’s now so easy to see what you haven’t got. Social media spreads images of excess abundantly and exuberantly. Sites such as Instagram elicit envy and distribute depression by allowing selfies to scream: “look at me! (and my oh so perfect life).” It’s all a lie, of course, but we don’t really notice this because the internet so easily becomes a prison of belief.

A narrowing of focus

In the Victorian era, when wealth was polarised, there was at least a shared moral code, broad sense of civic duty and collective responsibility. People, you might say, remained human. Nowadays, increasingly, individuals are looking out for themselves and digitalisation, true to form, is oiling the wheels of efficiency here too.

Individualism has created a culture that’s becoming increasingly venal, vindictive and avaricious. This isn’t just true in the West. In China there is anguished discussion about individual callousness and an emergent culture of compensation. The debate was initiated back in 2011 when a toddler, Yue Yue, was hit by several vehicles in Foshan, a rapidly growing city in Guangdong province, and a video of the event was posted online. Despite being clearly hurt no vehicles stopped and nobody bothered to help until a rubbish collector picked the child up. Yue Yue later died in hospital. Another incident, also in China, saw two boys attempting to save two girls from drowning. The boys failed and were made to pay compensation of around 50,000 Yuan (about £5,000) each to the parents for not saving them.

Such incidents are rare, but they are not unknown and do perhaps point toward a world that is becoming more interested in money than mankind – a world that is grasping and litigious, where trust and the principle of moral reciprocity are under threat. You can argue that we are only aware of such events due to digital connectivity, which is probably true, and that both sharing and volunteering are in good health. But you can also argue that the transparency conjured up by connectivity and social media is making people more nervous about sticking their necks out. In a word with no secrets, ubiquitous monitoring and perfect remembering people have a tendency to conform. Hence we click on petitions online rather than actually doing anything. I was innocently eating my breakfast recently when I noticed that Kellogg’s were in partnership with Chime for Change, an organisation committed to “raise funds and awareness for girls’ education and empowerment through projects promoting education, health and justice.” How were Kellogg’s supporting this? By asking people to share a selfie “to show your support.” To me this is an example of internet impatience and faux familiarity. It personifies the way that the internet encourages ephemeral acts of belonging that are actually nothing of the sort.

As for philanthropy, there’s a lot of it around, but much of it has become, as one Museum director rather succinctly put it: ‘money laundering for the soul.’ Philanthropy is becoming an offshoot of personal branding. It is buildings as giant selfies, rather than the selfless or anonymous love of humanity. One pleasing development that may offset this trend is crowd-funding, whereby individuals fund specific ideas with micro-donations. At the moment this is largely confined to inventions and the odd artistic endeavour, but there’s no reason why crowds of people with small donations can’t fund political or altruistic ideas or even interesting individuals with a promising future.

I sometimes wonder why we haven’t seen a new round of revolutions in the West. Due to digital media we all know all about the haves and the have yachts. It’s even easy to find out where the yachts are moored thanks to free tracking apps. Then again, we barely know our own neighbours these days, living, as we increasingly do, in digital bubbles where friends and news stories are filtered according to pre-selected criteria.

The result is that we know more and more about the people and things we like, but less and less about anything, or anyone, outside of our existing preferences and prejudices.

Putting aside cognitative biases such as inattentional blindness, which means we are often blissfully unaware of what’s happening in front of our own eyes, there’s also the thought that we’ve become so focussed on ourselves that focusing anger on a stranger five minutes up the road – or on a distant yacht – is a bit of stretch. This is especially true if you are addicted to 140 character updates of your daily existence or looking at photographs of cute cats online.

Mugged by reality

Is anyone out there thinking about how Marx’s theory of alienation might be linked to social stratification and an erosion of humanity? I doubt it, but the fall of Communism can be connected with the dominance of individualism and the emergence of self-obsession.

This is because before the fall of the Berlin Wall in 1989 there was an alternative ideology and economic system that acted as a counter-weight to the excesses of capitalism, free markets and individualism. Similarly, in many countries, an agile and attentive left took the sting out of any political right hooks. Then in the 1990s there was a dream called the internet. But the internet is fast becoming another ad-riddled venue for capitalism where, according to an early Facebook engineer (quoted by Ashlee Vance in his biography of Elon Musk) “the best minds of my generation are thinking about how to make people click ads.” The early dream of digital democracy has also soured because it turns out that a complete democracy of expression attracts voices that are “stupid, angry and have a lot of time on their hands.” This is a Jonathan Franzen again, although he reminds me of another writer, Terry Prachett, who pointed out that: “real stupidity beats artificial intelligence every time.”

To get back to the story in hand, the point here is that if you take away any balancing forces you not only end up with tax shy billionaires, but income polarisation and casino banking. You can also end up with systemic financial crashes, another of which will undoubtedly be along shortly, thanks to our stratospheric levels of debt, the globally connected nature of risk and the corruption and villainy endemic in emerging markets. It’s possible that connectivity will create calm rather than continued volatility, but I doubt it. More likely a relatively insignificant event, such as a modest rise in US interest rates, will spread panic and emotional contagion at which point anyone still living in a digital bubble will get mugged by reality.

Coming back to some good news, a significant economic trend is the growth of global incomes. This sounds at odds with declining real wages, but I am talking about emerging not developed markets. According to Ernst & Young, the accountancy firm, an additional 3 billion individuals are being added to the global middle class. That’s 3 billion more smart-phone using, FitBit wearing, Linked-in profiled, Apple iCar driving, Instagram obsessives.

In China, living standards have risen by an astonishing 10,000 per cent in a single generation. In terms of per capita GDP in China and India this has doubled in 16 and 12 years respectively. In the UK this took 153 years. This is pleasing, although the definition of middle class includes people earning as little as $10 a day. Many of these people also live behind the Great Firewall of China, so we shouldn’t get too carried away with trickle down economics or the opening up of democracy. What globalisation giveth to jobs automation may soon be taketh away too and many may find themselves sinking downward towards working class or neo-feudal status rather than effervescently rising upward.

According to Pew Research, the percentage of people in the US that think of themselves as middle class fell from 53 per cent in 2008 to 44 per cent in 2014, with 40 per cent now defining themselves as lower class compared to 25 per cent in 2008. Teachers, for example, that have studied hard, worked relentlessly and benefit society as a whole find themselves priced out of real-estate and various socio-economic classifications by the relentless rise of financial speculators. Deeper automation and virtualisation could make things worse. Martin Wolf, a Financial Times columnist, comments that intelligent machines ‘could hollow out middle class jobs and compound inequality.’

Even if the newfound global wealth isn’t temporary there’s plenty of research to suggest that as people grow richer they focus more attention on their own needs at the expense of others. So a wealthier world may turn out to be one that’s less caring.

Of course, it’s not numbers that matter. What counts are feelings, especially feelings related to the direction of travel. The perception in the West generally is that we are mostly moving in the wrong direction. This can be seen in areas such as education and health and it’s not too hard to imagine a future world split into two halves, a thin, rich, well-educated, mobile elite and an overweight, poorly educated, anchored underclass. This is reminiscent of HG Well’s intellectual, surface dwelling Eloi and downtrodden, subterranean Morlocks in The Time Machine and Tolkien’s Mines of Moria. The only difference this time might be that it’s the global rich that end up living underground, cocooned from the outside world in deep basement developments.

An upside to the downside

It’s obviously possible that this outcome is re-written. It’s entirely possible that we will experience a reversal where honour, spiritual service or courage to country are valued far above commerce. This is a situation that existed in Britain and elsewhere not that long ago. It’s possible that grace, humility, public spiritedness and contempt for vulgar displays of wealth could become dominant social values. Or perhaps a modest desire to leave as small a footprint as possible could become a key driving force.

On the other hand, perhaps a dark dose of gloom and doom is exactly what the world needs. Perhaps the era of cheap money is coming to an end and an extended period of slow growth will do us all a world a good. A study led by Heejung Park at UCLA found that the trend towards greater materialism and reduced empathy had been partly reversed due to the 2008-2010 economic downturn. In comparison with a similar study looking at the period 2004–2006, US adolescents were less concerned with owning expensive items, while the importance of having a job that’s ‘worthwhile to society’ rose. Whether this is just cyclical or part of a permanent shift is currently impossible to say.

These studies partly link with previous research suggesting that a decline in economic wealth promotes collectivism and perhaps with the idea that we only truly appreciate things when we are faced with their loss. There aren’t too many upsides to global pandemics, rogue asteroids and financial meltdowns, but the threat of impending death or disaster does focus the long lens of perspective, as Steve Jobs pointed out in his commencement speech at Stamford University.

Digital Vs Physical trust

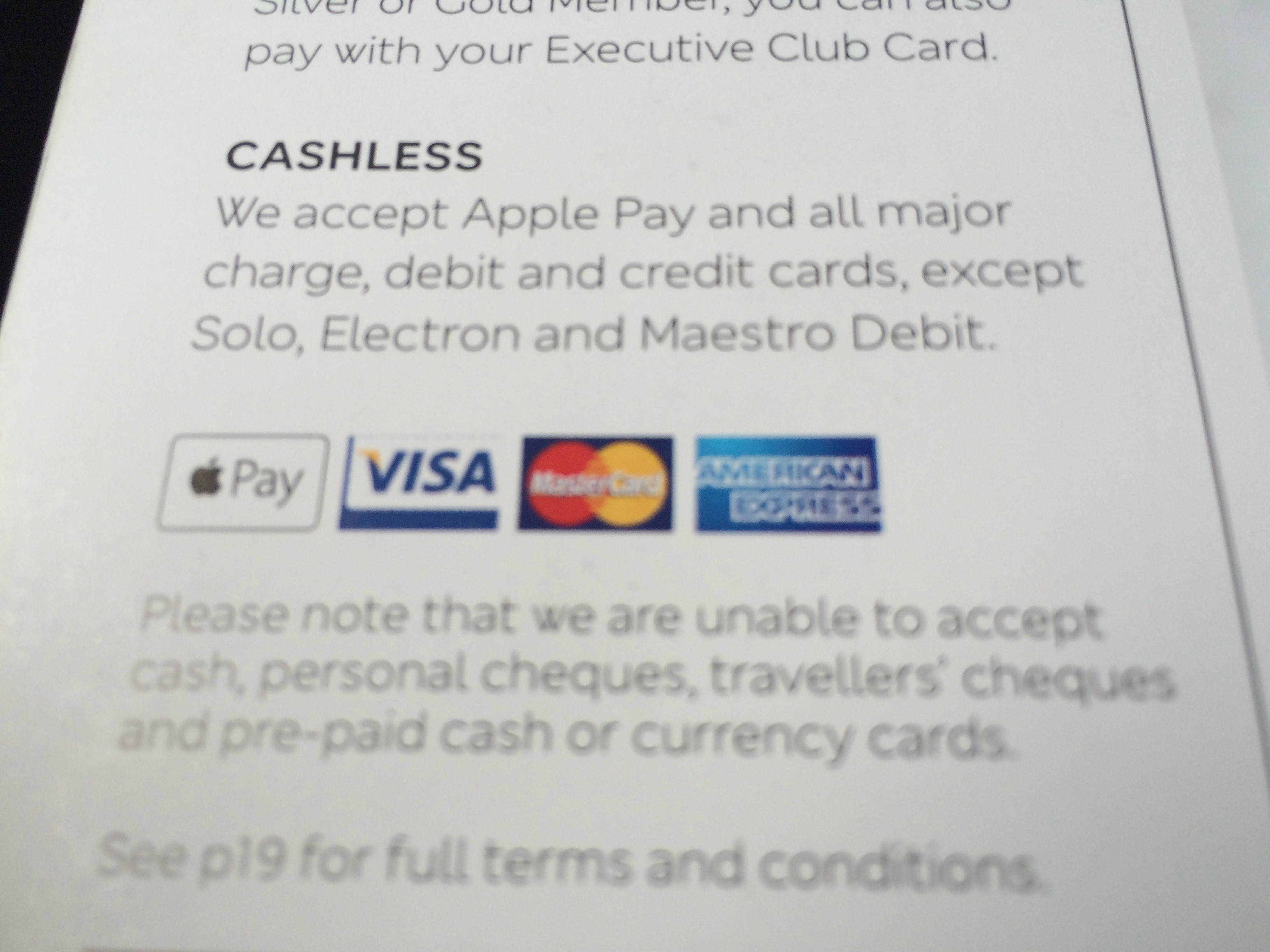

That’s enough about the economy. How might the digitalisation of money impact our everyday behaviour in the future? I think it is still too early to make any definitive statements about particular technologies or applications, but I do believe that the extinction of cash is inevitable because digital transactions are faster and more convenient, especially for companies. Cash can be cumbersome too. It’s also because governments and bureaucracies would like to reduce illegal economic activity and collect the largest amount of tax possible thereby increasing their power.

In the US, for instance, it’s been estimated that cash costs the American economy $200 billion a year, not just due to tax evasion and theft, but also due to time wasting. A study, by Tufts University says that the average American spends 28 minutes per month traveling to ATMs, to which my reaction is so what? What are people not doing by ‘wasting’ 28 minutes going to an ATM? Writing sonnets? Inventing a cure for cancer?

But a wholly cashless society, or global e-currency, won’t happen for a long time, partly because physical money, especially banknotes, is so tied up with notions of national identity (just look at the Euro to see how that can go wrong!). Physical money tells a rich story. It symbolises a nation’s heritage in a way that digital payments cannot. People in recent years have also tended to trust cash more. The physical presence of cash is deeply reassuring, especially in times of economic turmoil.

In the UK, in 2012, more than half of all transactions were cash and the use of banknotes and coins rose slightly from the previous year. Why? The answer is probably that in 2012 the UK was still belt-tightening and people felt they could control their spending more easily using cash. Or perhaps people didn’t trust the banks or each other. Similarly, in most rich countries, more than 90 per cent of all retail is still in physical rather than digital stores. We should also be careful not to assume that everyone is like ourselves. The people most likely to use cash are elderly, poor or vulnerable, so it would be a huge banking error, in my view, if everyone stopped accepting physical money. It’s also a useful Plan B to have a stash of cash in case the economy melts down or your phone battery dies leaving you with no way to pay for dinner. This is probably swimming against the tide though and I suspect there is huge pent-up demand for mobile and automated payments.

Globally cash is still king (85% of all transactions are still cash according to one recent study) but in developed economies this tends not to be the case. In the US about 60% of transactions are now digital, while in the UK non-cash payments have now overtaken physical cash. Money will clearly be made trying to get rid of physical money. According to the UK payments council the use of cash is expected to fall by a third by 2022. Nevertheless, circumstances do change and I suspect that any uptake of new payment technologies is scenario dependent.

I was on the Greek island of Hydra in 2014 and much to my surprise the entire economy had reverted to physical money. This was slightly annoying, because I had just written a blog post about the death of cash based on my experience of visiting the island two years earlier. On this visit almost everywhere accepted electronic payments, but things had dramatically changed. Again, why? I initially thought the reason was Greeks’ attempting to avoid tax. Cash is anonymous. But it transpired that the real reason was trust. If you are a small business supplying meat to a taverna and you’re worried about getting paid, you ask for cash. This is one reason why cash might endure longer than some e-evangelists tell us. Cash is a hugely convenient method to store and exchange value and has the distinct advantage of keeping our purchasing private. If we exchange physical cash for digital currency this makes it easier for companies and governments to spy on what we’re doing.

Countless types of cashless transactions

There are many varieties of digital money. We’ve had credit cards for a very long time. Transactions using cards have been digital for ages and contactless for a while. We’ve grown used to private currencies, virtual currencies, micro-payments, embedded value cards, micro-payments and contactless (NFC) payments. We’ve also learnt to trust PayPal and various Peer-to-Peer lending sites such as Zopa and Prosper, although one suspects that, like ATMs, we are happier taking money out than putting money in. We’re also slowly getting used to the idea of payments using mobile phones. There are even a few e-exhibitionists with currency chips embedded in their own bodies and while this might take a while to catch on I can see the value in carrying around money in our bodies. A chip inserted in your jaw or arm is a bit extreme, but how about a tiny e-pill loaded with digital cash that, once swallowed, is good for $500 or about a week? There’s even digital gold, but to be honest I can’t get my head around that at all. The key point here is that all of these methods of transaction are more or less unseen. They are also fast and convenient, which, I would suggest, means that spending will be more impulsive and less considered. We will have regular statements detailing our digital transactions, of course, but these will also be digital, delivered to our screens amid a deluge of other digital distractions and therefore widely ignored or not properly read.

Really thinking or mindlessly consuming?

What interests me most here is whether or not attitudes and behaviours change in the presence of invisible money. There is surprisingly little research on this subject, but what does exist, along with my own experience, suggests that once we shift from physical to digital money things do change.

With physical money (paper money, metal coins and cheques) we are more likely to buy into the illusion that money has inherent value. We are therefore more vigilant. In many cases, certainly my own, we are more careful. In short we think. Physical money feels real so our purchasing (and debt) is more considered. With digital money (everything from credit and debit cards to PayPal, Apple Money, iTunes vouchers, loyalty points and so forth) our spending is more impulsive. And as I said, earlier, when money is digital and belongs to someone else any careless behaviour is amplified.

Quantitative Easing (QE) is perhaps a similar story. If instead of pressing a key on a computer and sending digital money to a secondary market to buy financial assets including bonds we saw fleets of trucks outside central banks being loaded with piles of real money to do the same I suspect that our reaction would be wholly different. We might even question whether a government monetising (buying) its own debt is a sensible idea given that the 2008 financial meltdown was caused by the transmission and obfuscation of debt.

Of course, pumping money into assets via QE circles back to create inequality. If you own hard assets, such as real estate, then any price increases created by QE can be a good thing because it increases the value of your assets (often bought with debt, which is reduced via inflation). In contrast savers holding cash, or anyone without assets, is penalised.

It’s a bit of a stretch to link QE to the Arab Spring, but some people have, pointing out that food price inflation was a contributory factor, which can be indirectly linked to QEs effects on commodities. If one was a conspiracy theorist one might even suggest that QEs real aim was to drive down the value of the dollar, the pound and the Euro at the expense of spiralling hard currency debt and emerging economy currencies.

I’m getting back into macro-economics, which I don’t want to do, but it’s worth pointing out that in The Downfall of Money, the author Frederick Taylor notes that Germany’s hyperinflation not only destroyed the middle class, but democracy itself. As he writes, by the time inflation reached its zenith: ‘everyone wanted a dictatorship.’

The cause of Germany’s hyperinflation was initially Germany failing to keep up with payments due to France after WW1. But it was also caused by too much money chasing too few goods, which has shades of asset bubbles created by QE.

It was depression, not inflation per se, that pushed voters toward Hitler, but this has a familiar ring. Across Europe we are seeing a significant rightwards shift and one of the main reasons why Germany won’t boost the EU economy is because of the lasting trauma caused by inflation ninety years ago. If a lasting legacy of QE, debt, networked risk and a lack of financial restraint by individuals and institutions, all accentuated by digitalisation, is either high inflation or continued depression things could get nasty, in which case we might all long for the return of cash as a relatively safe and private way to endure the storm.

Crypto-currency accounts

The idea of a global digital economy that’s free from dishonest banks, avaricious speculators and regulation-fixated governments is becoming increasingly popular, especially, as you’d expect, online. Currencies around the world are still largely anchored to the idea of geographical boundaries and economies in which physical goods and services are exchanged. But what if someone invented a decentralised digital currency that operated independently of central banks? And what if that currency were to use encryption techniques, not only to ensure security and avoid confiscation or taxation, but to control the production of the currency? A crypto-currency like BitCoin perhaps?

In one scenario, BitCoin could become not only an alternative currency, but a stateless alternative payments infrastructure, competing against the like of Apple Pay and PayPal and against alternative currencies like airline miles. But there’s a more radical possibility.

What if a country got into trouble (Greece? Italy? Argentina?) and trust in the national currency collapsed. People might seek alternative ways to make payments or keep their money safe. If enough people flocked to something like BitCoin a government might be forced to follow suit and we’d end up with a crytocurrency being used for exports, with it’s value tied to a particular economy or set of economies.

More radically, how about a currency that rewarded certain kinds of behaviour? We have this already, in a sense, with loyalty cards, but I’m thinking of something more consequential. What if the underlying infrastructure of BitCoin was used to create a currency that was distributed to people behaving in a virtuous manner? What if, for instance, money could be earned by putting more energy or water into a local network than was taken out? Or how about earning money by abstaining from the development of triple sub-basements or by visiting an elderly person that lives alone and asking them how they are? We could even pay people who smiled at strangers using eye-tracking and facial recognition technology on Apple smart glasses or Google eye-contact lenses.

Given what governments would potentially be able to see and do if cash does disappear, such alternative currencies — along with old-fashioned bartering — could prove popular. At the moment, central banks use interest rates as the main weapon to control or stimulate the economy. But if people hoard cash because interest rates are low — or because they don’t trust banks — then the economy is stunted. But with a cashless society the government has another weapon in its arsenal.

What if banks not only charged people for holding money (negative interest rates) but governments imposed an additional levy for not spending it? This is making my head spin so we should move on to explore the brave new world of healthcare and medicine, of which money is an enabler. But before we do I’d like to take a brief look at pensions and taxation and then end on considering whether the likes of Mark Zuckerberg might actually be OK really.

If economic conditions are good, I’d imagine that money and payments will continue to migrate toward digital formats. Alternatives to banks will spring up and governments will loosen their tax-take. However, if austerity persists, or returns, then governments will do everything they can to get hold of more of your money — but they will be less inclined to spend it, especially on services. Taxation based upon income and expenditure will continue, but I expect that it will also shift towards assets and wealth and to a very real extent individual behaviour.

One of the effects of moving toward digital payments and connectivity is transparency. Governments will, in theory, be able to see what you’re spending your money on, but also how you’re living in a broader sense. Hence stealth taxation. Have you put the wrong type of plastic in the recycling bin again? That’s a fine (tax). Kids late for school again? Fine (tax). Burger and large fries again? You get the idea… Governments will seek to not only maximise revenue, but nudge people toward certain allegedly virtuous behaviours and people will be forced to pay for the tiniest transgressions. This, no doubt, will spark rage and rebellion, but they’ll be a tax for that too.

As for pensions, there are several plausible scenarios, but business as usual doesn’t appear to be one of them. The system is a pyramid-selling scheme that’s largely bust and needs to be reinvented in many countries. 1 in 7 people in the UK has no retirement savings whatsoever, for instance, and the culture of instant digital gratification would suggest that trying to get people to save a little for later won’t meet with much success.

What comes next largely depends on whether the culture of now persists and whether or not responsibility for the future is shared individually or collectively. If the culture of individualism and instant rewards holds firm, we’ll end up with a very low safety net or a situation where people never fully retire. If we are able to delay gratification, we’ll end up either with a return to a savings culture or one where the state provides significant support in return for significant contributions. The bottom line here is that pensions are set firmly in the future and while we like thinking about the future we don’t like paying for it. So what might happen that could change the world for the better and make things slightly more sustainable?

An economy if people still matter

In 1973, the economist EF Schumacher’s book Small is Beautiful warned against the dangers of ‘gigantism.’ On one level the book was a pessimistic polemic about modernity in general and globalisation in particular. On the other hand it was possibly prescient and predictive. Schumacher foresaw the problem of resource constraints and foreshadowed the issue of human happiness, which he believed could not be sated by material possessions.

He also argued for human satisfaction and pleasure to be central to all work, mirroring the thoughts of William Morris and the Arts and Crafts Movement. They argued that since consumer demand was such a central driver of the economy, then one way to change the world for the better would be to change what the majority of people want, which links directly back into money and our current voracious appetite for material possessions.

On one level Schumacher’s book is still an idealistic hippy homily. On another it manages to describe our enduring desire for human scale, human relationships and technology that is appropriate, controllable and above all understandable. Physical money encourages the physical interaction of people, whereas digital cash is more hands off and remote. Digital transactions require energy and while any desire for green computing won’t exactly stop the idea of a cashless society in its tracks it may yet restrain it.

There are already some weak signals around this, which Schumacher may have approved of. Our desire for neo-Victorian computing (Steam Punk), craft sites like Etsy, the popularity of live music events and literature festivals and digital detoxing all point to a desire for balance and a world where humans are allowed to focus on what they do best. The partly generational shift toward temporary digital access rather than full physical ownership is also an encouraging development against what might be termed stuffocation.

Schumacher also warned against the concentration of economic and political power, which he believed would lead to dehumanisation. Decisions should therefore be made on the basis of human needs rather than the revenue requirements of distantly accountable corporations and governments. In this respect the internet could go either way. It could bring people together and enable a more locally focussed and sustainable way or living or it could facilitate the growth of autocratic governments and monopolistic transnational corporations. But remember that the dematerialisation of the global economy – the analogue to digital switch if you will – is largely unseen and therefore mostly out of mind so very few people are discussing this at the moment.

To some extent digital payments are a technology in search of a problem. Cash is easy to carry, easy to use and doesn’t require a power source – except to retrieve it from an ATM. Meanwhile credit and debit cards are widely accepted worldwide and online, so why do we need additional channels or formats? Maybe we don’t. Maybe we don’t even need money as much as we think. One of the problems with the digital economy from an economics standpoint is that digital companies don’t produce many jobs. But maybe this isn’t a problem. Once we’ve achieved shelter and security and managed to feed ourselves, the things that make us happy tend to be invisible to economists. The things that fulfil our deepest human needs are not to be physical things, but nebulous notions like love, belonging and compassion. This is reminiscent of Abraham Maslow’s hierarchy of needs, but unfortunately self-esteem, altruism, purpose and spirituality don’t directly contribute to GDP or mass employment. Perhaps they should.

It pains me to say it, but maybe the digital dreamers are onto something after all. Maybe the digital economy will change our frame of reference and focus our attention on non-monetary value and human exchange even if this goes a little crazy at times.

What would Schumacher make our current economic situation? Maybe he’d see the present day as the start of something nasty. Maybe he’d see it as the start of something beautiful. What I suspect he would point out is that many people feel that they have lost control of their lives, especially financially. Job insecurity, austerity, debt and a lack of secure saving and pensions make people anxious. This can have physical effects. According to a study published in the medical magazine The Lancet, economic conditions can make people and their genetic dependants sick. Putting to one side the increased risk of suicide, mental health is a major casualty of volatile economic and geopolitical conditions. Psychological stress means that our bodies are flooded with stress hormones and these can make us ill.

Turbulent economic conditions can also make long lasting changes to our genes, which can be a catalyst for heart disease, cancer and depression in later generations. Another study, co-led by George Slavich at the University of California at Los Angeles, says that there is historical evidence for such claims and cites the fact that generations born during recessions tend to have unusually short lifespans. Research by Jenny Tung at Duke University in North Carolina also suggests that if animals perceive they have a lower social rank, the more active their pro-inflammatory genes become. This may be applicable to humans perceiving that they are becoming digital-serfs. Even the anticipation of bad news or negative events may trigger such changes, which might explain why I recently heard that the shark in Notting Hill is now on medication.