“It is a fatal fault to reason without observing, though so necessary beforehand and useful afterwards” – Charles Darwin.

Quote time

Reply

“It is a fatal fault to reason without observing, though so necessary beforehand and useful afterwards” – Charles Darwin.

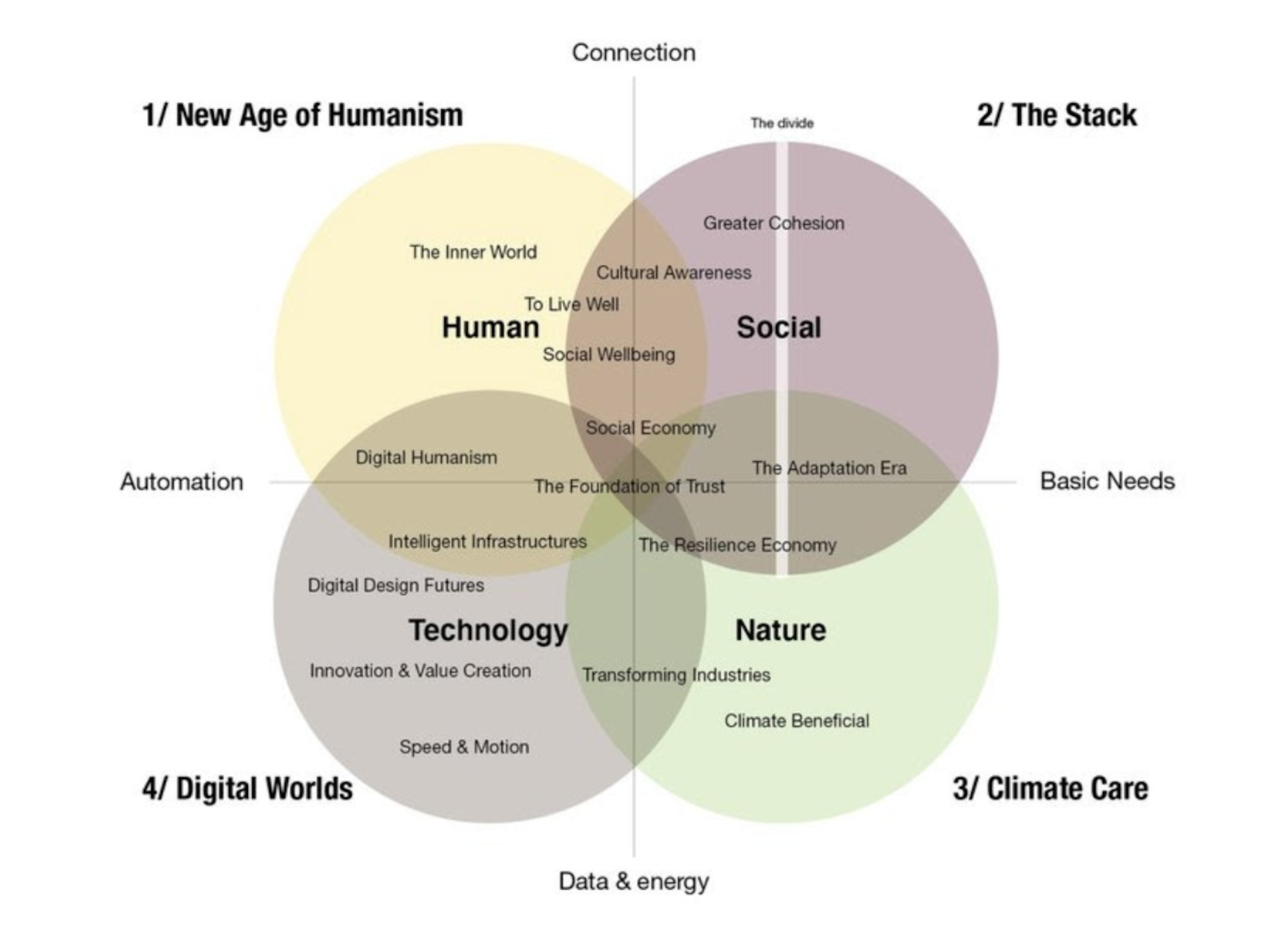

Maybe it’s me, but I don’t understand this, especially the axes. It’s from Oltmans van Niekerk, a global research and innovation firm in the Netherlands.

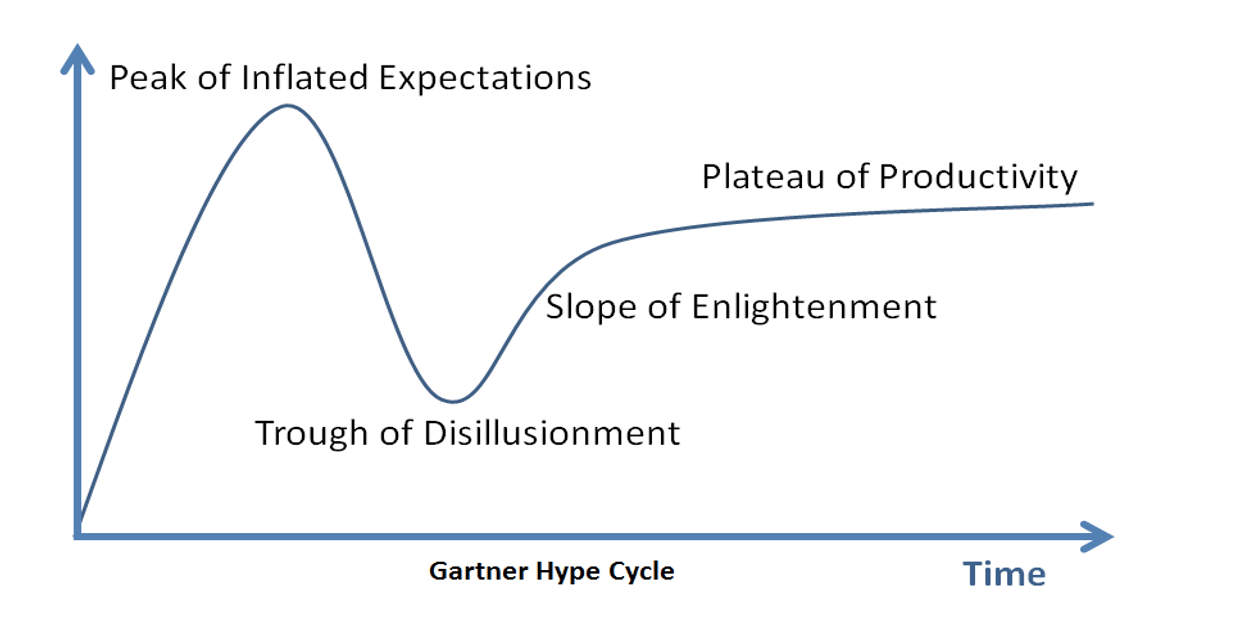

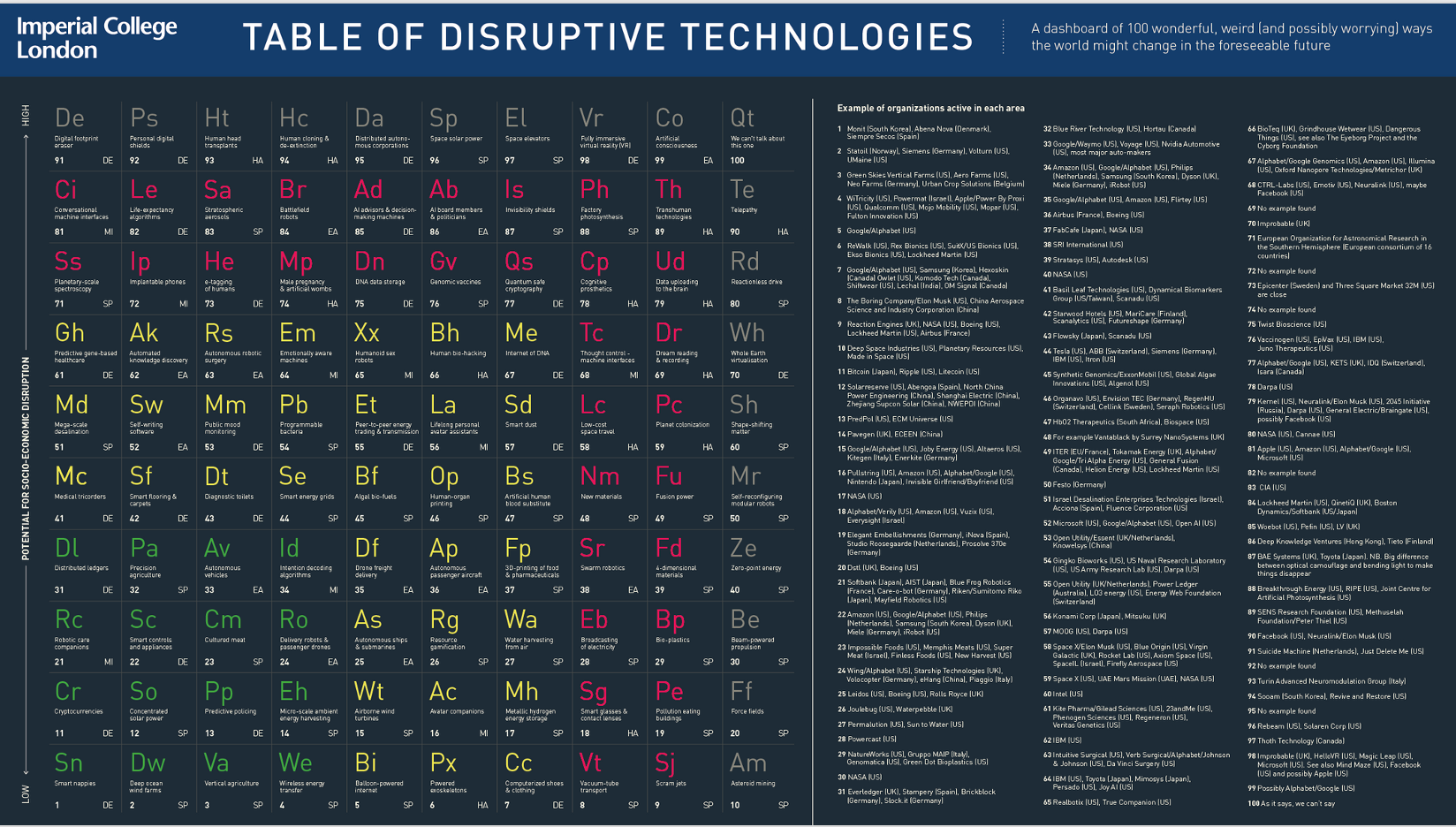

Where have I been? LinkedIn mainly. I will try to be here more often in the future. Much to post, but let’s start with this article about when innovations succeeed – or fall flat. Best read having looked at Gartner’s Hype Cycle and my own Table of Disruptive Terchnologies.

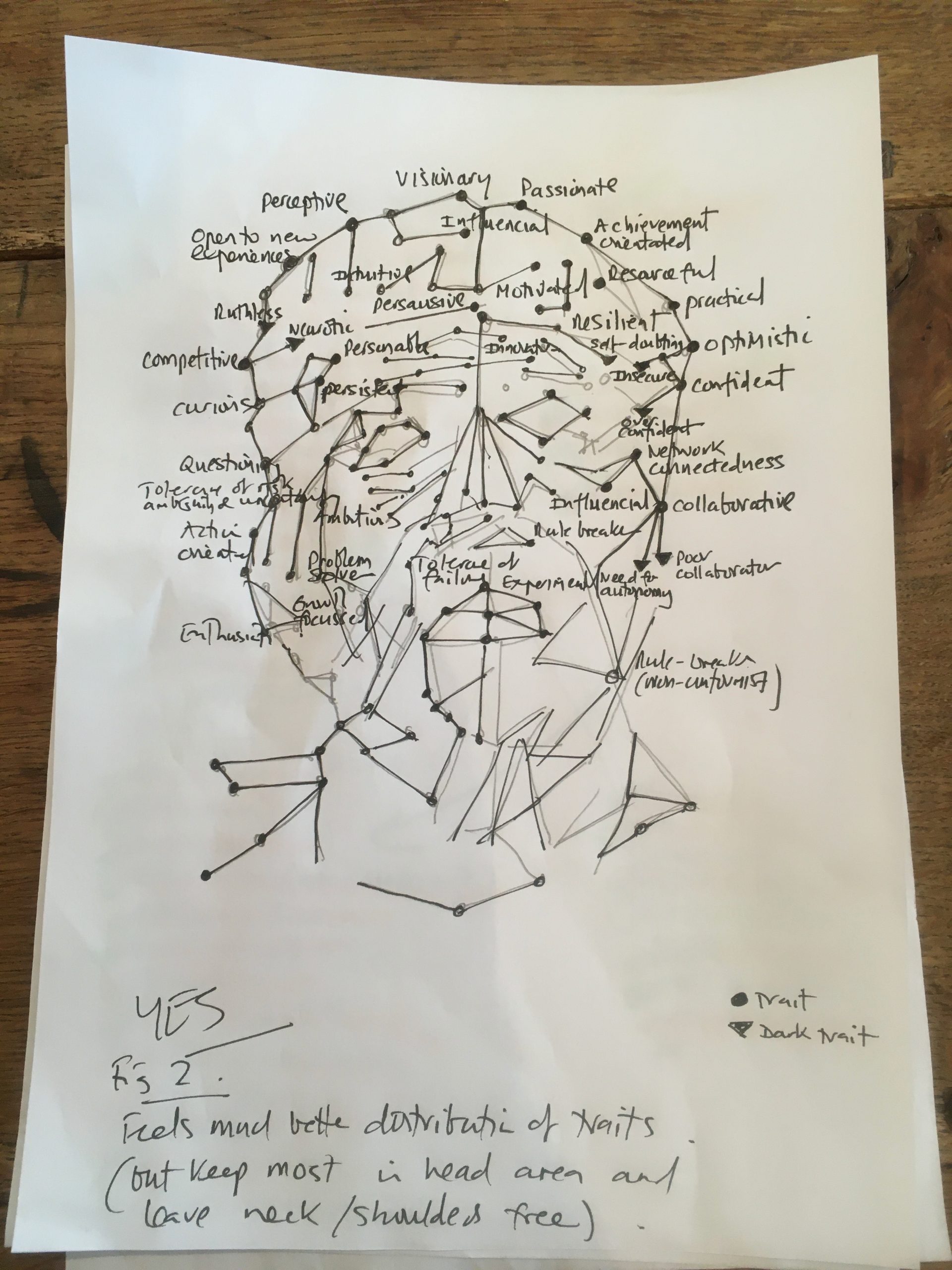

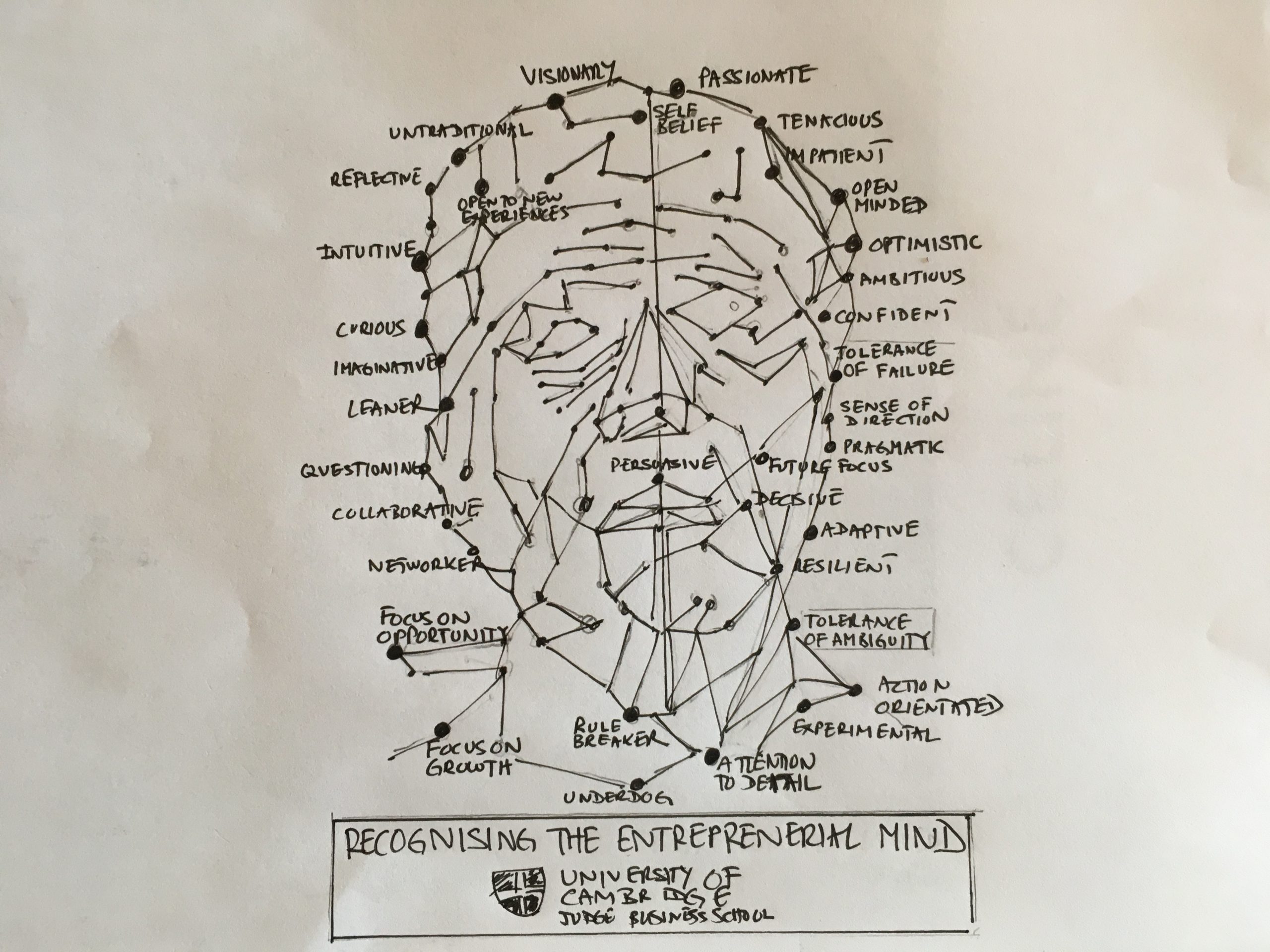

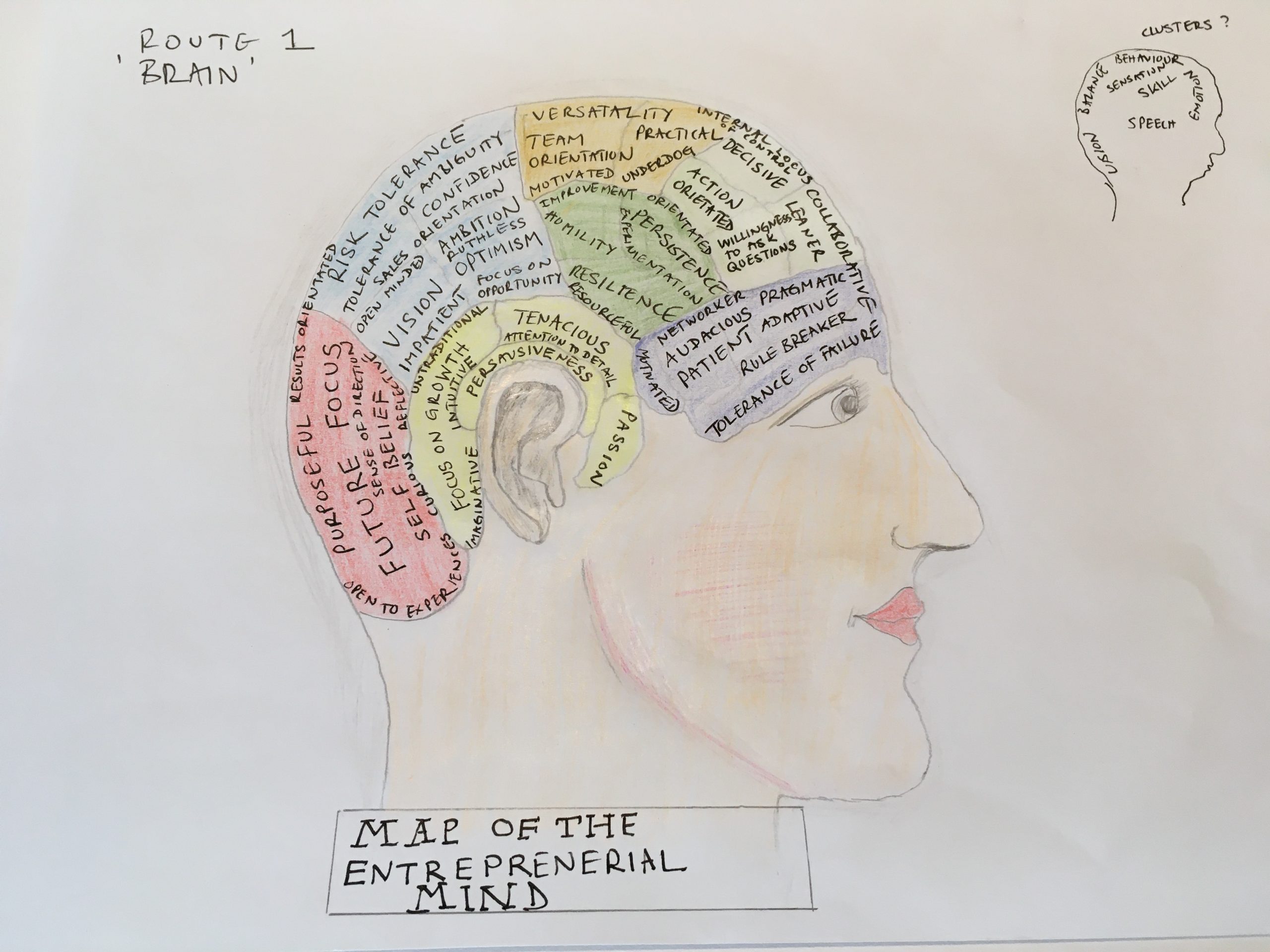

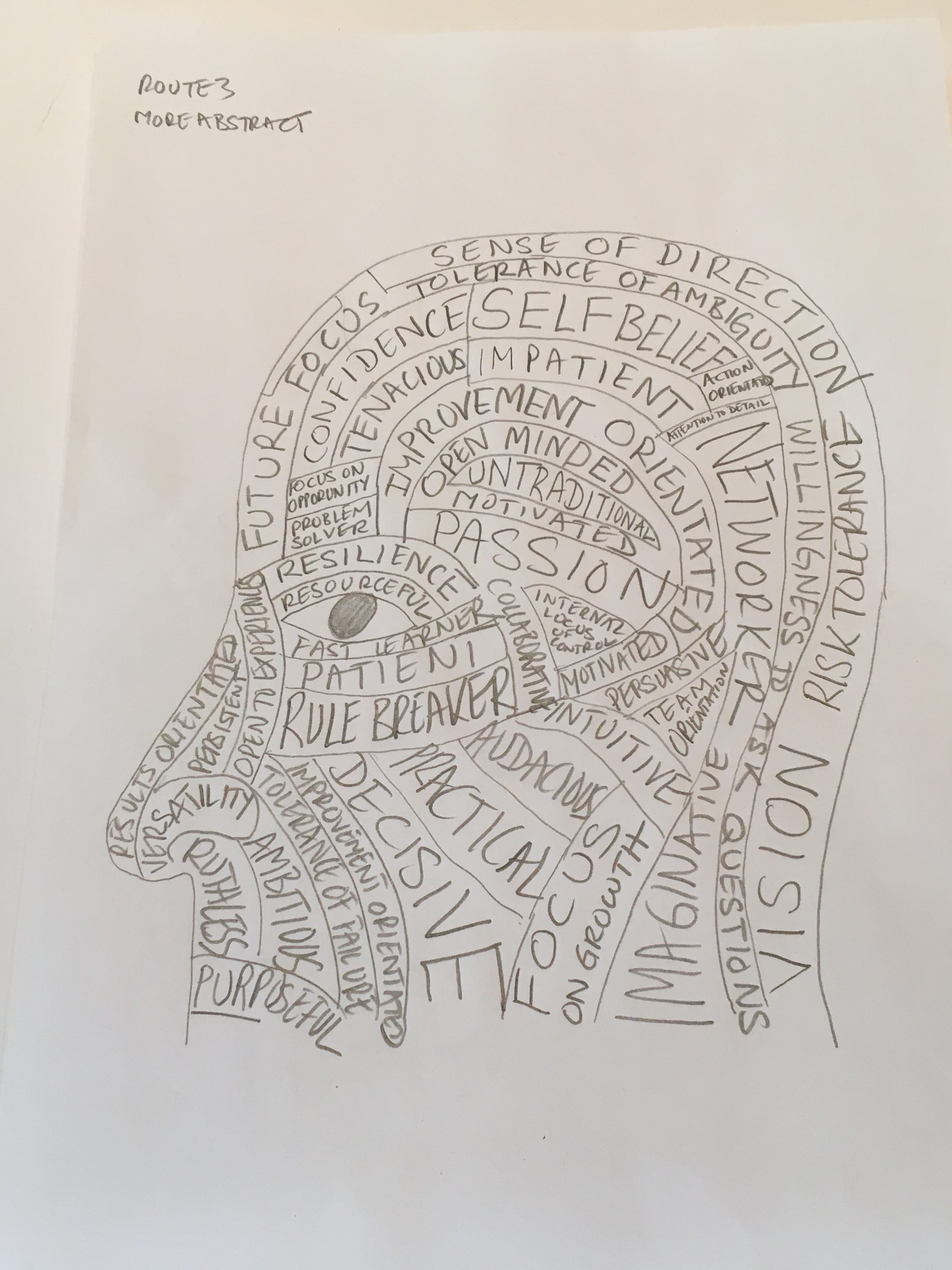

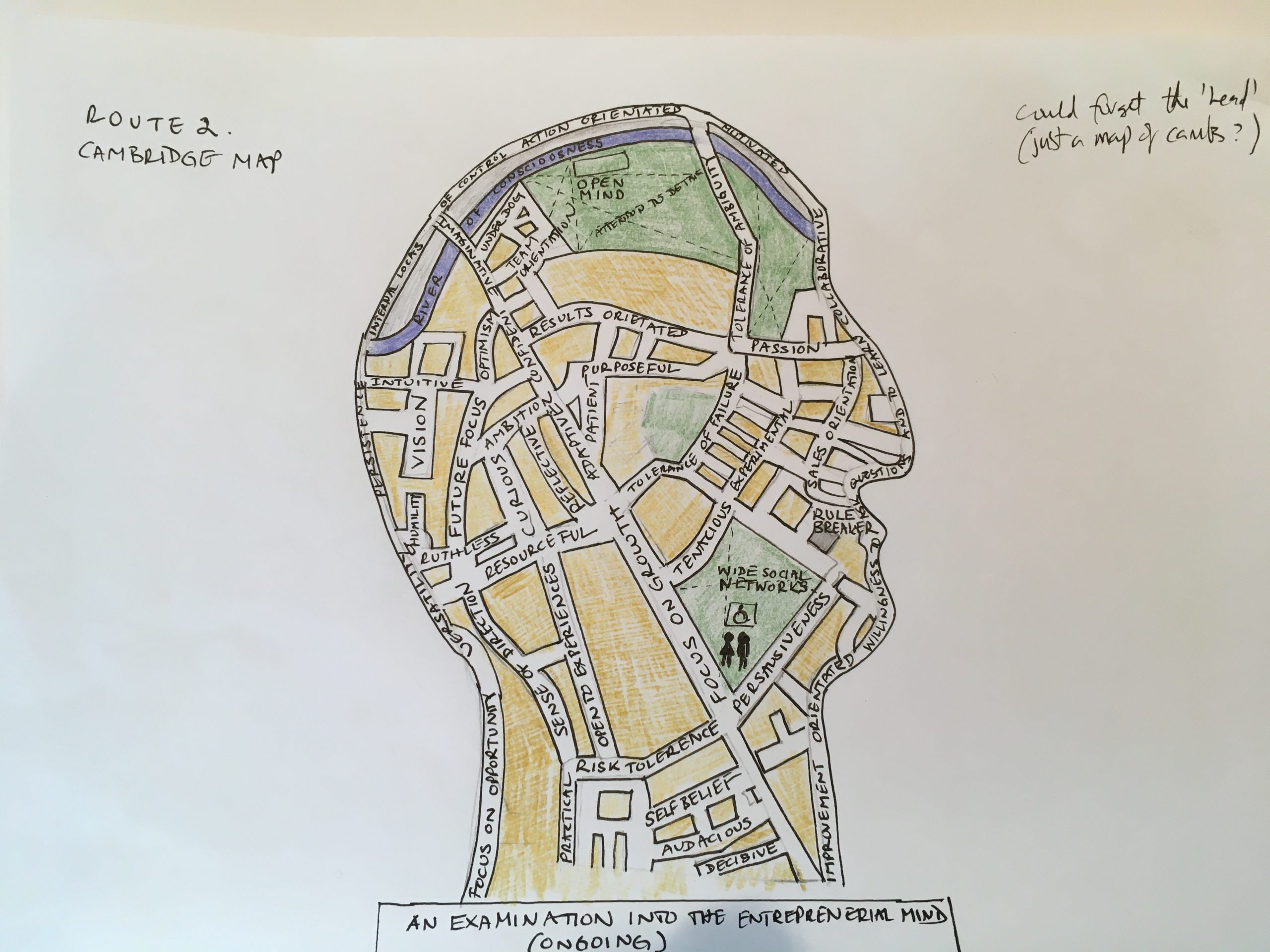

This one has been a while coming. It’s a visual exploration of some of the traits and states associated with an entreprenerial mind. Obviously not everyone will possess all of these traits or states and neither are they static – these will change over time too as a start-up grows and new people join the business. Perhaps a question is which states work best throughout an organisations lifecycle?

Bibliography:

Peta Levi, ‘Flourishing in the Cambridge parkland’, Financial Times, November 1980

Segal Quince Wicksteed, The Cambridge Phenomenon: The Growth of High Technology Industry in a University Town, 1985

Lyle M. and Signe M. Spencer, Competence at work: models for superior performance (Chapter 17, Entrepreneurs), John Wiley & Sons, Inc., 1993

Sally Caird, What do psychological tests suggest about entrepreneurs? Journal of Managerial Psychology, 8(6) pp. 11–20, 1993

Tom Byers (Stanford), Heleen Kist (Stanford) and Robert I. Sutton (Hass), Characteristics of the Entrepreneur: Social Creatures, Not Solo Heroes, Handbook of Technology Management, Richard C. Dorf (Ed), CRC Press, October 1997

Yin M. Myint, Shailendra Vyakarnam and Mary J. New, The effect of social capital in new venture creation: the Cambridge high‐technology cluster, John Wiley & Sons, June 2005

S Kavadias, SC Sommer, The effects of problem structure and team diversity on brainstorming effectiveness, Management Science, 2009

T Miller, M Grimes, J McMullen and T Vogus, Venturing for others with heart and head: How compassion encourages social entrepreneurship, Academy of Management Review 37 (4), 616-640, 2012

J Hutchison‐Krupat, RO Chao, Tolerance for failure and incentives for collaborative innovation, Production and Operations Management, 2014

The Cambridge Phenomenon: 50 Years of Innovation and Enterprise, Kate Kirk and Charles Cotton, Third Millennium, 2012

M. Frese & M. M. Gielnik, The psychology of entrepreneurship. Annual Review of Organizational Psychology and Organizational Behavior, 1, 413–438, 2014

M. J. Gorgievski & U. Stephan, Advancing the Psychology of Entrepreneurship: A Review of the Psychological Literature and an Introduction. Applied Psychology, 65(3), 437–468, 2016

Lynda Applegate, Janet Kraus, and Timothy Butler, Skills and Behaviors that Make Entrepreneurs Successful, HBR Working Knowledge, June 2016

Dean A. Shepherd and Holger Patzelt, Entrepreneurial Cognition: Exploring the Mindset of Entrepreneurs, Palgrave Macmillan, 2018

Nicos Nicolaou, Phillip H. Phan and Ute Stephan, The Biological Perspective in Entrepreneurship Research, Entrepreneurship Theory and Practice, November 2020

Early roughs…

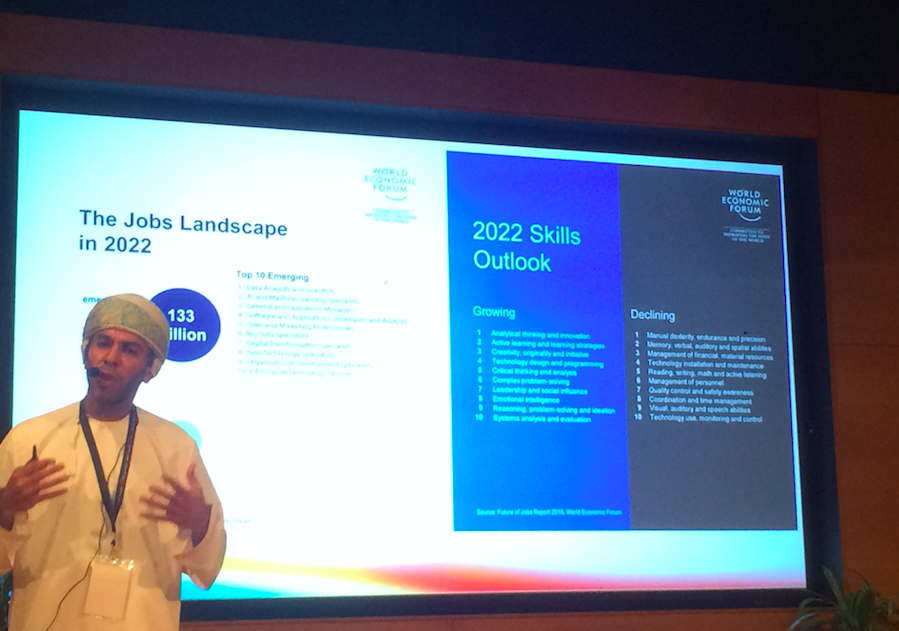

I’m in Oman speaking at a technology conference organised by Bank Muscat. But here’s the thing. I was doing some background homework on Oman, especially on the future of Oman. This got me looking at a project called Oman 2040 (also mentioned at the conference). Looking into this further I got into future skills and education (a subject very close to my heart – my mother was a teacher). Anyway, quite separately I’m supposed to be writing something on the future of universities for publication in Australia (I get around!). I’ve been stuck on this for weeks to the point where I was about to say that I couldn’t do it. But then two things happened (and I think this is how ideas hatch generally, which links to innovation and, serendipitously, another conference in Oman called the Global Innovation Summit. (Stay with me here it’s going somewhere).

Last week I was at another conference on AI at Cambridge (like I said, I get around). By total fluke I sat next to a film maker at dinner. (I tried to sit next to a few other people, but they told me to move!). Anyway, the film maker and I got talking about education and he mentioned the 4-Cs of education (Critical thinking, Communication, Collaboration and Creativity). So that idea got stuck in my subconscious.

Then today I was having dinner by myself in Muscat and after eating I had a cigar (known as a ‘thinking stick’ to a salesman from IBM that I once met). Then out of nowhere I had an idea. The 4C’s are all wrong*. It should be the Seven Cs. They should be: Collaboration, Creativity, Critical Thinking, Communication, Curiosity, Compassion (EQ) and (Moral) Character.

So, there you have it folks. That’s how ideas get born. My essay on the future of universities is now flowing like there’s no tomorrow…

Can biology teach us anything about innovation? The essence of Darwinism is that progress is created by adaptation to changing circumstances. What starts off as a random mutation often spreads throughout a population to eventually become the norm through a process of natural selection. The same is surely true with innovation. New ideas are mutations created through chaos and adaptation, especially when two or more old ideas combine or reproduce in unusual or unexpected ways. In short, innovation = inheritance (history) + variation + selection.

Serendipity clearly plays an important part in this process and the list of things created by accident is certainly impressive; Aspirin, Band-Aids, credit cards, DNA finger printing, dynamite, inoculation, Jell-O, Ferrari, Lamborghini, microwave ovens, penicillin, ink-jet printers, X-rays, nylon, heart pacemakers, Coca-Cola, Teflon, Vulcanised rubber, Nintendo, Lego, Smart Dust, matches, dynamite (yikes), safety glass, Corn Flakes, Super Glue, Viagra and Velcro to name quite a few.

Pursuing experiments – and tolerating the inevitable failures that result – is therefore one practical way to make an organisation more innovative. But is there is another option? Is there a strategy, process or even a culture that will embed innovative thinking at the very core of an organisation’s being? I think there is.

Think about when individuals and institutions are at their most innovative. You might think about the cross-fertilisation of disciplines and experience. This is indeed one way to kick-start innovative thinking and it’s not that difficult to design spaces where diverse people will bump into each other in a random manner. Office kitchens and staircases immediately spring to mind. Lunch is even better. A Harvard Business Review article once claimed that P&G had attempted to “systemise the serendipity” that so often sparks innovation. When the Hollywood producer Brian Grazer heard about this he commented: “that’s what we call lunch.”

Another route is to combine the energy and naivety of youth with the wisdom and cynicism of old age. This can work too. Reverse mentoring is a very practical idea championed by the likes of former GE boss Jack Welsh. Or there’s the thought of recruiting both the newest and the oldest members of staff for brainstorms. Diversity in terms of skills is key, but so too are age and experience.

And, of course, there’s the idea that if you generate enough ideas one will surely be good enough to use. This does occasionally work, although in my experience not very often. I prefer the opposite, which involves thinking inside a small box rather than thinking outside of one. Read, for example, Adam Morgan’s book called A Beautiful Constraint.*

So, what’s my big idea for generating big ideas? What’s my million- dollar idea? Death. That’s right, demise, departure, disappearance, extinction, the grim reaper. Hold on, am I seriously suggesting that we kill companies and organisations just to reinvent them?

Sort of.

It strikes me that true clarity only arrives occasionally and generally it’s when we think we are going to die. If we are looking down the barrel of a gun – or a microscope – we tend to see our death (and with it our entire life) in high definition. This creates a tremendous sense of urgency to put it mildly. This might not be of much use if we have seconds to live, but if we are given weeks or months we’re often able to focus on the things we really want to do and separate what’s merely urgent from what’s actually important. Relationships are rekindled, ideas are hatched, things get reinvented.

Sometimes we are fortunate. We think we are going to die, but we don’t. The tests or the analysis were wrong. The threat failed to materialise. We were lucky. Sometimes the change resulting from serious threats is enduring, although more often than not we revert to our bad old ways once the grim reaper has gone elsewhere. This is true for institutions as much as it’s true for individuals.

One of the reasons that Apple, sometimes cited as the world’s most valuable company, is so innovative might be to do with the fact it was 90 days away from being bankrupt back in 1997. Similar near death experiences abound, ranging from Telsa, SpaceX and KFC to Airbnb, FedEx and IBM.

So, the second million-dollar question must surely be this…can you fake your own death in order to think straight or to become more innovative? Believe it or not a company in South Korea once tried to do precisely this, although it backfired somewhat.

Back in 2008 there was a South Korean craze called ‘well-dying’ in which employees would write and then read out their last words in fake funeral services. Organisations such as Samsung and Hyundai sent their employees on courses organised by Korea Life Consulting in order to question their life paths and priorities. The idea got a lot of bad press at the time, partly because people were required to get inside a real coffin, but it wasn’t a wholly bad idea.

Asking people what they’d do if they had a day, a week or a year left to live can be a good way to reveal what they really think about things, including themselves. Asking a leadership team inside a large organisation to do the same is a similarly good way to reveal not only priorities, but potentially to revaluate strategies too. What might you do differently if you didn’t have to worry about regulation, unions, governments, quarterly earnings and so forth?

After all, if you have absolutely nothing to lose you will behave very differently than if you do. You will try things that are riskier and be far less concerned with what others might think of you. In short, you will be brave and be led by your heart as much as your head. You’ll dream big and be less inclined to get stuck on practicalities.And, of course, we only truly appreciate what we have been given when there’s a real chance that these same things will be taken away. It is only through death that we really learn to live.

As Charles Darwin said: “It is not the strongest of the species that survives, nor the most intelligent, but the one most responsive to change.” Try using a narrative of rapidly changing circumstances and ultimately the imminent extinction of your organisation to radically revaluate where you are going and how you might get there.Or write an obituary for your organisation and then treat it as a strategy for reincarnation.

Carpe diem.

* A Beautiful Constraint: How to transfer your limitations into advantages, and why it’s everyone’s business by Adam Morgan

Can biology teach us anything about innovation? The essence of Darwinism is that progress is created by adaptation to changing circumstances. What starts off as a random mutation often spreads throughout a population to eventually become the norm through a process of natural selection. The same is surely true with innovation. New ideas are mutations created through chaos and adaptation, especially when two or more old ideas combine or reproduce in unusual or unexpected ways.

Serendipity clearly plays an important part in this process and the list of things created by accident is certainly impressive; Aspirin, Band-Aids, credit cards, DNA finger printing, dynamite, inoculation, Jell-O, Ferrari, Lamborghini, microwave ovens, penicillin, ink-jet printers, X-rays, nylon, heart pacemakers, Coca-Cola, Teflon, Vulcanised rubber, Nintendo, Lego, Smart Dust, matches, dynamite (yikes), safety glass, Corn Flakes, Super Glue, Viagra and Velcro to name quite a few.

Pursuing experiments – and tolerating the inevitable failures that result – is therefore one practical way to make an organisation more innovative. But is there is another option? Is there a strategy, process or even a culture that will embed innovative thinking at the very core of an organisation’s being? I think there is.

Think about when individuals and institutions are at their most innovative. You might think about the cross-fertilisation of disciplines and experience. This is indeed one way to kick-start innovative thinking and it’s not that difficult to design spaces where diverse people will bump into each other in a random manner. Office kitchens and staircases immediately spring to mind. Lunch is even better. A Harvard Business Review article once claimed that P&G had attempted to “systemise the serendipity” that so often sparks innovation. When the Hollywood producer Brian Grazer heard about this he commented: “that’s what we call lunch.”

Another route is to combine the energy and naivety of youth with the wisdom and cynicism of old age. This can work too. Reverse mentoring is a very practical idea championed by the likes of former GE boss Jack Welsh. Or there’s the thought of recruiting both the newest and the oldest members of staff for brainstorms. Diversity in terms of skills is key, but so too are age and experience.

And, of course, there’s the idea that if you generate enough ideas one will surely be good enough to use. This does occasionally work, although in my experience not very often. I prefer the opposite, which involves thinking inside a small box rather than thinking outside of one. Read, for example, Adam Morgan’s book called A Beautiful Constraint.*

So, what’s my big idea for generating big ideas? What’s my million- dollar idea? Death. That’s right, demise, departure, disappearance, extinction, the grim reaper. Hold on, am I seriously suggesting that we kill companies and organisations just to reinvent them?

Sort of.

It strikes me that true clarity only arrives occasionally and generally it’s when we think we are going to die. If we are looking down the barrel of a gun – or a microscope – we tend to see our death (and with it our entire life) in high definition. This creates a tremendous sense of urgency to put it mildly. This might not be of much use if we have seconds to live, but if we are given weeks or months we’re often able to focus on the things we really want to do and separate what’s merely urgent from what’s actually important. Relationships are rekindled, ideas are hatched, things get reinvented.

Sometimes we are fortunate. We think we are going to die, but we don’t. The tests or the analysis were wrong. The threat failed to materialise. We were lucky. Sometimes the change resulting from serious threats is enduring, although more often than not we revert to our bad old ways once the grim reaper has gone elsewhere. This is true for institutions as much as it’s true for individuals.

One of the reasons that Apple, sometimes cited as the world’s most valuable company, is so innovative might be to do with the fact it was 90 days away from being bankrupt back in 1997. Similar near death experiences abound, ranging from Telsa, SpaceX and KFC to Airbnb, FedEx and IBM.

So, the second million-dollar question must surely be this…can you fake your own death in order to think straight or to become more innovative? Believe it or not a company in South Korea once tried to do precisely this, although it backfired somewhat.

Back in 2008 there was a South Korean craze called ‘well-dying’ in which employees would write and then read out their last words in fake funeral services. Organisations such as Samsung and Hyundai sent their employees on courses organised by Korea Life Consulting in order to question their life paths and priorities. The idea got a lot of bad press at the time, partly because people were required to get inside a real coffin, but it wasn’t a wholly bad idea.

Asking people what they’d do if they had a day, a week or a year left to live can be a good way to reveal what they really think about things, including themselves. Asking a leadership team inside a large organisation to do the same is a similarly good way to reveal not only priorities, but potentially to revaluate strategies too. What might you do differently if you didn’t have to worry about regulation, unions, governments, quarterly earnings and so forth?

After all, if you have absolutely nothing to lose you will behave very differently than if you do. You will try things that are riskier and be far less concerned with what others might think of you. In short, you will be brave and be led by your heart as much as your head. You’ll dream big and be less inclined to get stuck on practicalities.And, of course, we only truly appreciate what we have been given when there’s a real chance that these same things will be taken away. It is only through death that we really learn to live.

As Charles Darwin said: “It is not the strongest of the species that survives, nor the most intelligent, but the one most responsive to change.” Try using a narrative of rapidly changing circumstances and ultimately the imminent extinction of your organisation to radically revaluate where you are going and how you might get there.

Write an obituary for your organisation and then treat it as a strategy for reincarnation.

Carpe diem.

* A Beautiful Constraint: How to transfer your limitations into advantages, and why it’s everyone’s business by Adam Morgan

“And what was the true object of this superstitious stuff? A final clue came from “Creativity: Flow and the Psychology of Discovery and Invention” (1996), in which Mihaly Csikszentmihalyi acknowledges that, far from being an act of individual inspiration, what we call creativity is simply an expression of professional consensus. Using Vincent van Gogh as an example, the author declares that the artist’s “creativity came into being when a sufficient number of art experts felt that his paintings had something important to contribute to the domain of art.” Innovation, that is, exists only when the correctly credentialed hivemind agrees that it does. And “without such a response,” the author continues, “van Gogh would have remained what he was, a disturbed man who painted strange canvases.” What determines “creativity,” in other words, is the very faction it’s supposedly rebelling against: established expertise.”

Taken from Salon, ‘TED talks are lying to you’ by Thomas Frank

(Article originally published in Harper’s)

I’m starting to think about my next book and although the illusion of progress is a fairly tempting title there’s the danger of it being mistaken for a negative position (actually the positive impact of negative thinking is interesting theme in itself). So, alternatively, I’ve been thinking again about thinking. What influences it? How can we increase the quantity and, more importantly, the quality of our thinking?

I’ve been thinking about this sitting in my favourite chair, in my greenhouse, drinking red wine and smoking a cigar.

Why is it that the average lifespan of an S&P 500 company in the US has fallen from 67 years in the 1920s to just 15 years today? And why might 75% of firms in the S&P 500 now be gone or going by the year 2027 or thereabouts?

These figures come from a study by Richard Foster at the Yale School of Management and echo another from the Santa Fe Institute that found that publically quoted firms die at similar rates regardless of age or industry sector. In this second study the average lifespan of American companies was cited at just 10 years. The reason given for most of these companies dying or disappearing is a merger or acquisition.* A third US study** of S&P companies reports an average company age of 61 in 1958, 25 in 1980 and around 18 today, but the trend toward shorter lives remains regardless of which study you read.

In the UK it’s a similar story. Of the 100 companies in the FTSE 100 in 1984, only 24 were still breathing in 2012, although average corporate lifespans in the UK were somewhat longer. However, with start-ups it’s back to bleak, with almost 50% of SMEs failing to celebrate their 5th birthday. The reasons UK start-ups fail are said to include cash flow issues, a lack of bank lending, too much red tape, high business rates and competition.

With larger enterprises in the UK and elsewhere the situation can be somewhat different. The main reason that big companies die – beyond being consumed by larger or more aggressive companies – is that they fail to anticipate or react to new technology, new customer demands or competitors with new business models, products and services, all of which are often linked and can cause considerable disruption and disturbance.

This is Darwinian evolution applied to capitalism and the only solution is to keep your eyes and ears wide open for predators and to continually evolve what you do through a process of constant adaption and occasionally accelerated mutation.

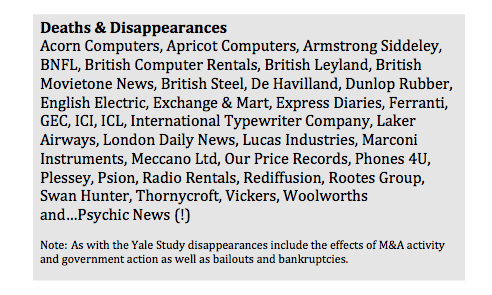

The list of corporate casualties is certainly long. Most people are aware of how things developed at Kodak, but the list of companies killed off or seriously injured by new technologies, new competitors or new customer behaviours includes a roll call of previously proud British names including Ferranti, Psion, Acorn Computers, De Havilland, British Leyland, British Steel, ICI, Marconi, Swan Hunter, Armstrong Siddeley, GEC and ICL.

Interestingly, in each case the writing was on the wall long before many of these companies went bankrupt or were taken over, but if there’s one thing that you can rely on with big companies it’s that, like super-tankers, they can take a long time to change direction and the view from the bridge is often partially obscured or heavily contested.

Nothing recedes like Success

Putting to one side new technologies, new competition and new customer demands, a key point is geriatric corporate cultures. Bill Gates once said that “success is a lousy teacher, it seduces smart people into thinking they can’t lose.” In other words, nothing recedes quite like success and large companies can become delusional about their fitness, their intellect or the speed and energy with which new ideas and inventions can move.

If arrogance is one silent killer, another is that as companies grow and become bigger management can become distanced from both insight and innovation. Peter Drucker made this point decades ago, although he used the word entrepreneurship. Managing and innovating are different dimensions of the same task, but most large companies regard them as separate to the point of putting them in different departments or locations. As the urgency to stay alive financially evaporates the focus shifts away from urgent opportunities and threats to lethargic internal issues and a kind of corporate immune system develops whereby new ideas tend to be rejected by the corporate body the minute they form.

If you drop down the organisation chart to departments such as customer complaints this isn’t always the case. People working in customer relations, IT, sales or even accounts can be extremely close to customers, and hence to the inception of new ideas, but senior management often writes off these departments as cost centres rather than hotbeds of insight and innovation. With R&D it’s often much the same story with scientists and engineers being regarded as grey suited bureaucrats offering up ponderous improvements rather than white-coated warriors fighting for discoveries that could transform the company.

The culture of organisations contributes to failure in other ways too. The dominant culture of most very large companies is highly conservative and quite rightly so. Publically quoted firms primarily exist to provide a regular return to shareholders and to keep workers in regular employment. But to do both these things they must also deliver constantly evolving products that create value for customers.

This is like a tightrope that’s not only swaying in the wind, but is being constantly moved and adjusted at one end while you’re still walking along it. Interestingly, Mark Vergano, an executive VP at Du Pont once made a similar point with regard to R&D saying that: “Research and development is always a delicate balance between maintaining a long-term view and remaining sensitive to short-term financial objectives.”

To sum up, if companies wish to remain healthy and grow old they need to do two things. Firstly, they need to remain young at heart. They need to remain mentally agile, constantly learn new things and question their own identity and reason for being.

This means repeatedly asking what business they’re really in and how best they can serve both current and future customers using current and future technologies, channels and business models.

Secondly, companies must look at innovation from a whole business perspective and make innovation truly cross-functional. If innovation exists purely at a departmental, product or service level it’s unlikely to proceed beyond incremental refinement. Continuous improvement is essential, but it’s merely a ticket to stay in the game. To win the game companies must consider more radical developments including the ground up reinvention of everything they do and also link innovation to strategy.

Three quick ways to extend the lifespan of your company:

1. Constantly look out for and test new ideas that could breathe new life into your company or fatally wound it if applied by a competitor.

2. In a similar vein don’t simply keep an eye on what your closest competitors are doing, also study what small start-ups outside your immediate market or geography are doing too. Are they doing anything unusual? Are they doing anything that doesn’t immediately make sense? If so dig into why.

3. Keep a close eye on what your youngest customers and employees are doing. What are they doing that you aren’t? Could such behaviour be an early warning signal of change?

Footnotes.

* A merger or acquisition isn’t necessarily a business failure, but can nevertheless be a sign of weakness or long-term illness.

**Innosight study (US).

If you’re wondering, the world’s oldest limited liability corporation is Enso Stora, a Finnish paper and pulp manufacturer that started out as a mining company in 1288.

{kind=link}